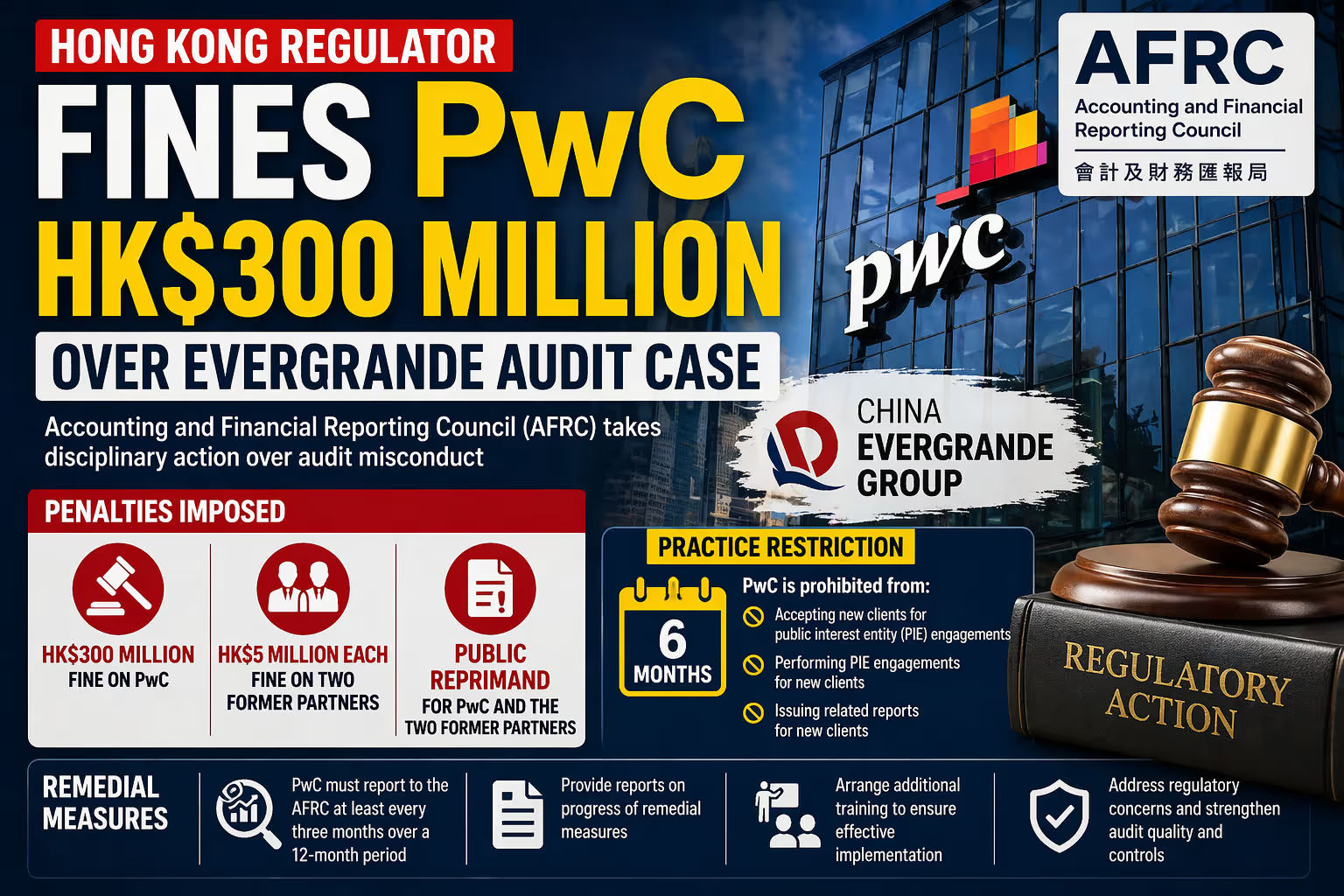

HK Accounting Watchdog Penalises PwC HK$300 Million, Enforces Six-Month Practice Ban Over Evergrande Audit

Hong Kong Accounting Regulator Fines PwC HK$310 Million and Imposes Practice Restrictions Over Evergrande Audit Case

Hong Kong’s accounting regulator, the Accounting and Financial Reporting Council (AFRC), has taken one of its most significant disciplinary actions in recent years by penalising global audit firm PricewaterhouseCoopers (PwC) and two of its former senior partners over misconduct linked to the audit of China Evergrande Group’s consolidated financial statements.

The case has drawn widespread attention across financial markets, regulatory circles, and the accounting profession because it concerns one of the world’s largest corporate collapses and raises serious questions about audit quality, professional scepticism, and the responsibilities of major accounting firms.

Under the announced action, the AFRC publicly reprimanded PwC and two former engagement leaders, imposed total fines of HK$310 million, and introduced a six-month restriction preventing PwC from taking on certain new public-interest audit engagements in Hong Kong.

The decision marks a major development in regulatory oversight and signals stronger enforcement standards for auditors involved in high-risk and high-profile corporate cases.

What Action Has Been Taken?

According to the regulator, the disciplinary package includes:

HK$300 million fine on PwC

HK$5 million fine each on two former PwC partners

Public reprimand of PwC and the two former partners

Six-month immediate practice restriction on PwC

Mandatory remedial reporting and training obligations

The combined penalty totals HK$310 million, making it one of the most substantial sanctions ever imposed on an accounting firm in the Hong Kong market.

What Does the Practice Restriction Mean?

In addition to the monetary penalty, the AFRC imposed an immediate six-month practice restriction on PwC.

During this period, PwC cannot:

Accept new clients for public interest entity (PIE) engagements

Perform PIE engagements for new clients

Issue related reports for such new clients

This restriction is highly significant because public interest entities generally include listed companies, financial institutions, insurers, and other organisations whose financial reporting is considered important to investors and the broader public.

While PwC can continue serving existing eligible clients subject to applicable rules, the inability to onboard certain new clients for six months could have commercial, reputational, and competitive consequences.

Why This Case Matters

The case centres on the audit of China Evergrande Group, once one of China’s largest property developers. Evergrande became globally known after suffering a severe debt crisis, triggering concerns over China’s real estate sector, creditor exposure, unfinished housing projects, and financial contagion risks.

Because Evergrande had massive liabilities and complex financial structures, the accuracy of its audited financial statements became critically important to:

Shareholders

Bondholders

Banks and lenders

Regulators

Credit rating agencies

Global investors

When a company of that size faces financial distress, scrutiny often turns to whether warning signs should have been identified earlier by management, boards, auditors, and regulators.

Role of Auditors in Such Cases

External auditors are appointed to independently examine whether a company’s financial statements present a true and fair view under applicable accounting standards.

Auditors are not expected to guarantee that a company will never fail. However, they are expected to:

Test evidence supporting reported figures

Challenge management assumptions

Assess internal controls

Evaluate risks of fraud or misstatement

Consider going-concern issues

Maintain independence and scepticism

In large and highly leveraged companies, these responsibilities become even more critical.

The AFRC’s action suggests that, in its view, serious shortcomings occurred in how the relevant audits were conducted.

Why Evergrande Was a High-Risk Audit

Evergrande was not an ordinary corporate client. It operated in a sector known for:

Heavy debt financing

Large land banks

Complex project accounting

Revenue recognition judgments

Asset valuation challenges

Cash flow dependency

Related-party risks

Refinancing pressure

For such businesses, auditors typically need to apply enhanced procedures and greater scepticism.

Any weakness in testing assumptions, verifying balances, or responding to risk indicators can become highly consequential.

Public Reprimand: More Than Symbolic

The AFRC also publicly reprimanded PwC and the two former partners. A public reprimand is more than a symbolic step—it formally records regulatory misconduct and can materially affect trust, brand perception, and future business opportunities.

For global professional firms, reputation is one of the most valuable assets. Even where financial penalties are manageable, reputational damage can have longer-lasting effects.

Why the Fine Is Significant

PwC is one of the “Big Four” global accounting firms, alongside Deloitte, EY, and KPMG.

Large multinational firms generate substantial revenues, so regulators often calibrate fines at levels intended to be meaningful enough to deter misconduct.

A HK$300 million penalty indicates the regulator viewed the matter as serious and deserving of a strong enforcement response.

It also sends a message to the broader audit industry that failures in major public-interest audits may attract severe sanctions.

Why Former Partners Were Also Penalised

The two former partners and engagement directors were each fined HK$5 million.

This highlights an important regulatory principle: accountability does not stop at the firm level. Senior individuals responsible for leading audits may also face personal consequences where misconduct or serious failures are found.

That approach is increasingly common globally, as regulators seek to strengthen individual accountability rather than relying solely on corporate penalties.

Remedial Measures Ordered

The AFRC did not stop at punishment. It also ordered corrective measures.

PwC must:

Report progress at least every three months over a 12-month period

Provide formal updates to the regulator

Arrange additional training

Demonstrate implementation of remedial controls

This reflects a broader regulatory philosophy: enforcement should improve future audit quality, not merely punish past failures.

Likely focus areas for remediation may include:

Audit documentation standards

Risk escalation processes

Partner supervision

Independence safeguards

Technical review procedures

High-risk client acceptance controls

Quality management systems

Wider Impact on the Audit Profession

This case is likely to resonate far beyond Hong Kong.

Audit regulators in many jurisdictions have become more assertive after major corporate collapses worldwide, including cases involving construction firms, retailers, finance companies, and property developers.

Common themes include:

Did auditors challenge management enough?

Were warning signs ignored?

Was revenue overstated?

Were valuations realistic?

Were going-concern issues properly considered?

The PwC case reinforces the trend toward stricter oversight of large accounting firms.

Market Implications

For listed companies and financial institutions seeking auditors, the case may influence future decisions regarding:

Audit firm selection

Audit committee scrutiny

Fee negotiations

Governance expectations

Quality assurance demands

Boards may increasingly ask tougher questions of auditors, particularly in sectors exposed to leverage, real estate, or complex accounting estimates.

Hong Kong’s Regulatory Reputation

Hong Kong is a major international financial centre. Strong financial reporting oversight is essential to maintaining investor confidence.

By taking visible enforcement action in a high-profile case, the AFRC may be seeking to demonstrate that Hong Kong applies robust regulatory standards and is prepared to hold major global firms accountable.

This can be important for:

International investors

Capital markets credibility

Cross-border listings

Governance rankings

Trust in audited accounts

Challenges Facing Large Audit Firms

The case also reflects broader structural challenges in auditing large multinational clients:

Complexity of Global Businesses

Large corporations often operate through hundreds of subsidiaries across multiple jurisdictions.

Time Pressure

Financial statements must be completed within reporting deadlines.

Commercial Tensions

Audit firms must remain independent while maintaining client relationships.

Talent and Expertise Needs

Complex audits require specialised sector knowledge and experienced staff.

Fraud Detection Expectations

Public expectations often exceed formal audit scope.

Regulators increasingly expect firms to overcome these challenges through better systems and stronger culture.

Lessons for Corporate Boards

Boards and audit committees should not treat an external audit as a substitute for internal governance.

They should ensure:

Strong internal controls

Independent audit committees

Reliable financial reporting systems

Open communication with auditors

Early escalation of risks

A quality audit works best when governance inside the company is also robust.

Lessons for Investors

Investors often rely heavily on audited accounts. However, this case is a reminder that audits are important—but not infallible.

Investors should also examine:

Debt levels

Cash flow trends

Governance quality

Business model sustainability

Sector conditions

Management credibility

Independent analysis remains essential.

What Happens Next for PwC?

PwC will now likely focus on:

Compliance with the restriction order

Internal review of affected practices

Engagement with regulators

Staff training and quality upgrades

Rebuilding trust with clients and markets

As a global network, PwC has deep resources and established systems, but regulatory events of this scale typically prompt significant internal reforms.

Conclusion

The AFRC’s decision to fine PwC HK$310 million and impose a six-month practice restriction over the Evergrande audit is a landmark enforcement action in Hong Kong’s accounting sector.

It reflects growing regulatory intolerance for audit failures in major public-interest cases and underscores the importance of scepticism, independence, and quality control in external audits.

For the accounting profession, the message is clear: large brand names do not shield firms or individuals from accountability. For markets, the case reinforces that credible oversight remains essential to investor confidence.

As regulators worldwide intensify scrutiny of auditors, this decision may become a reference point for future enforcement actions across global financial centres.

Related Posts

नयाँ आर्थिक ऐन लागू: निजी विद्यालय र अस्पतालमा ३% शुल्क, आयकरदेखि बिजुली र सेयर करसम्म के–के फेरियो?

चालु आर्थिक वर्षदेखि लागू भएको नयाँ आर्थिक ऐनले नेपालको कर प्रणालीमा ठूलो परिवर्तन गरेको छ। निजी शिक्षा र स्वास्थ्य सेवामा ३% इक्विटी शुल्क, नयाँ आयकर स्ल्याब, बिजुलीमा VAT, सेयर तथा घरजग्गाको पुँजीगत लाभकर वृद्धि, डिजिटल भुक्तानीमा VAT हटाउने र स्टार्टअपलाई पाँच वर्ष आयकर छुट दिने व्यवस्था लागू भएको छ।